☐ ☐ ☒ ☐ ☐ Prologis, Inc.(Name of Person(s) Filing Proxy Statement, if other than the Registrant)Payment of Filing Fee (Check the appropriate box):☒ ☐ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1)Title of each class of securities to which transaction applies:(2)Aggregate number of securities to which transaction applies:(3)Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):(4)Proposed maximum aggregate value of transaction:(5)Total fee paid:☐materials.materials

Notice of of | ||||

AHEAD OF WHAT’S NEXT™

Prologis Proxy Statement

Notice of annual meeting of stockholders

Prologis Park Ontario, Ontario, California

Thursday, April 29, 2021

1:30 p.m., Pacific time

The date of this proxy statement is March 19, 2021

Notice of 2021 Annual Meetingof Stockholders

March 19, 2021

To our stockholders:

I invite you to attend the 20212023 annual meeting of stockholders of Prologis, Inc. at 1:30 p.m. on April 29, 2021. Due to the COVID-19 outbreak and to support the health and well-being of our stockholders, directors and employees, ourMay 4, 2023. Our annual meeting will be held in a virtual format only. You will not be able to attend the annual meeting physically.

Items of business. The following items of business will be conducted at our 20212023 annual meeting of stockholders:

| 1. | Elect eleven directors to our Board to serve until the next annual meeting of stockholders and until their successors are duly elected and qualified. | |

| 2. | Advisory vote to approve the company’s executive compensation for | |

| 3. | Advisory vote on the frequency of future advisory votes on the company’s executive compensation. |

| 4. | Ratify the appointment of KPMG LLP as our independent registered public accounting firm for the year | |

| 5. | Consider any other matters that may properly come before the meeting and at any adjournments or postponements of the meeting. |

| Record Date. If you were a holder of shares of our common stock at the close of business on March | How to Vote. You can vote your shares by proxy through the Internet, by telephone or by mail using the instructions on the proxy card or you can vote during the virtual annual meeting. Any proxy may be revoked in the manner described in the accompanying proxy statement at any time prior to its exercise at the annual meeting. | Meeting Attendance. To be admitted to the annual meeting at |

Proxy Materials. On or about March 19, 2021,24, 2023, we intend to distribute to our stockholders:

| (i) | Either in printed form by mail or electronically by email, a Notice of Annual Meeting and Internet Availability of Proxy Materials containing instructions on: (a) how to electronically access our |

| (ii) | If requested or required, printed proxy materials, which will include our |

On behalf of the Board of Directors,

EDWARD S. NEKRITZ Chief Legal Officer, General Counsel and Secretary |

Important Notice Regarding the Availability of Proxy Materials for the Annual Meeting of Stockholders to be held on

|

|

|

Table of Contents |

This proxy statement contains important information for you to consider when deciding how to vote on the matters brought before the Annual Meetingannual meeting of the Stockholders. Please read it carefully.

The following summary highlights information contained in this proxy statement. This summary does not contain all the information you should consider and you should read the entire proxy statement before voting. For more complete information regarding our 20202022 performance, please review our Annual Report on Form 10-K for the year ended December 31, 2020.2022. All company operational information in this proxy statement is for the year ended or as of December 31, 2020,2022, unless otherwise noted. See Appendix A for definitions and discussion of non-GAAP measures and reconciliations to GAAP measures and for additional detail regarding definitions of terms as generally explained in the proxy statement. References in this proxy statement to “we,” “us,” “our,” the “company,” and “Prologis” refer to Prologis, Inc. and its subsidiaries, unless the context otherwise requires.

Our Business HighlightsModel Delivers Long-Term Growth Across Cycles

Our business model delivers long-term growth and outperformance.

In 2020,2022, we stood resilient through the pandemic, outperforming both operationally anddelivered strong operational performance in the equity markets for yet another successful year.face of volatile macroeconomic circumstances, which continued our industry outperformance and earned record Promote income from our Strategic Capital business.

Financial Performance |

Strategic Capital is a Powerful Differentiator | |

|

|

Prologis Datteln Distribution Center 1, Datteln, Germany

| (1) |

|

|

|

The |

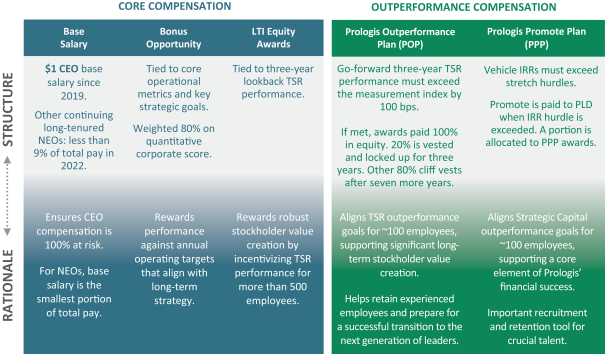

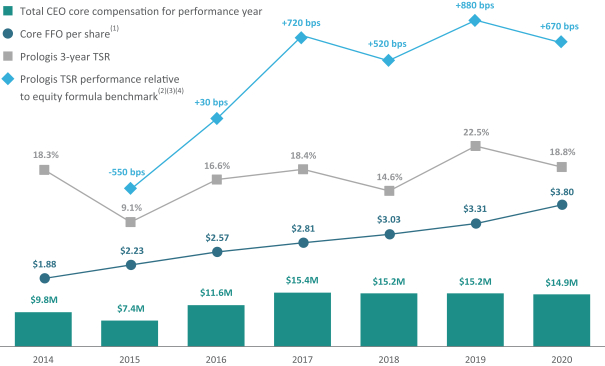

For further detail, please see “Compensation Discussion and Analysis.”

|

1

|

2020 2022 COMPENSATION HIGHLIGHTS

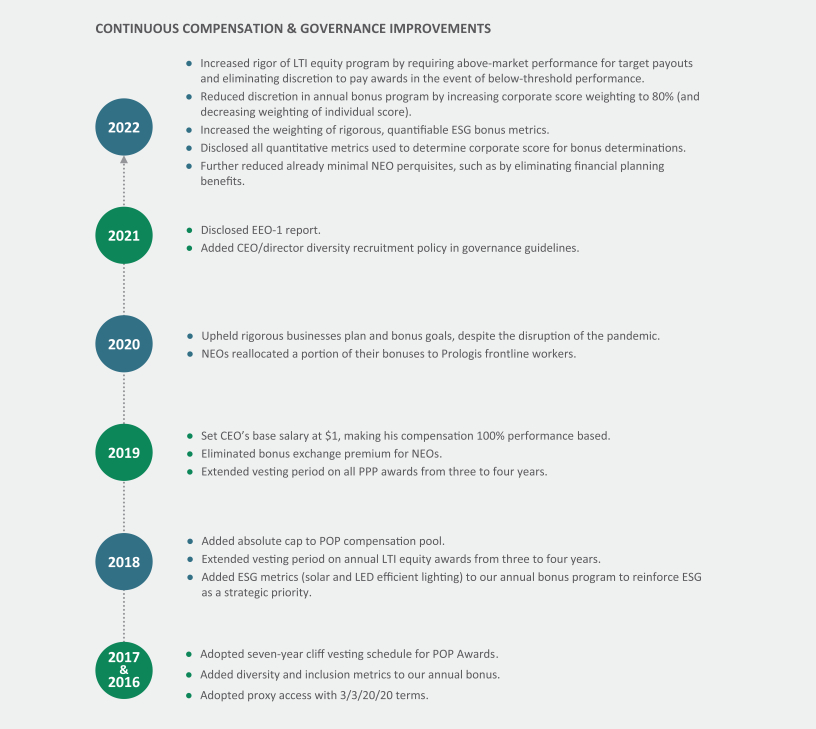

Compensation HighlightsProgram Improvements

OurIn response to stockholder feedback, we adopted various improvements to our compensation program, rewards for performance.including:

| Prologis Promote Program (PPP) | NEO Succession Planning | |

and regarding future Promote earning opportunities. |

to be commensurate with new executives’ tenure and |

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 2 |

| PROXY SUMMARY |

Prologis Elizabeth Seaport, Elizabeth, New Jersey

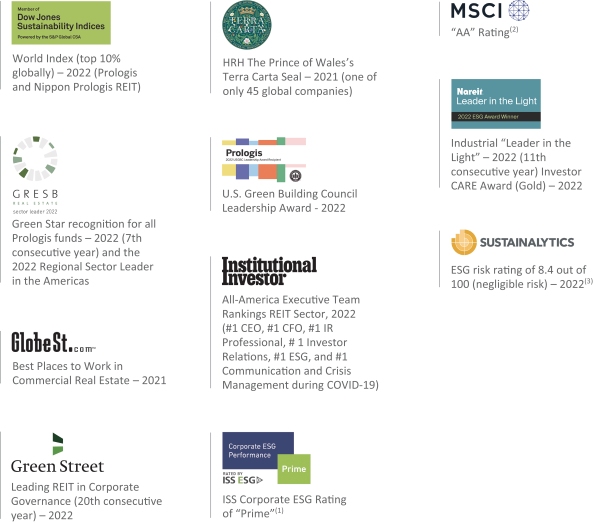

2022 ENVIRONMENTAL, SOCIAL AND GOVERNANCE (ESG) HIGHLIGHTS

We Have a Long-Standing Record of ESG Leadership

By 2040 | #1 in ESG The top REIT ESG program by Institutional Investor 2022. | |

Commitment, announced in 2022, | ||

20 Consecutive Years

|

|

2020 Environmental Stewardship, Social Responsibility and Governance (ESG) Highlights

We have a long-standing commitment to ESG leadership.

|

| |

A leading REIT in corporate by Green |

Global sustainable companies

| |

Nanjing Airport Logistics Center, Nanjing, China

For further detail, please see “Board of Directors and Corporate |

|

3

|

Proposals Submitted to Vote at the 20212023 Annual Meeting

We are asking our stockholders of record on March 7, 2023, to vote on the following matters at our 2023 annual meeting of stockholders to be held on May 4, 2023. Please see the section entitled “Additional Information” for details on how to vote and the vote required to approve these matters.

|

Proposal | Board Recommendation | ||||

PROPOSAL 1:Election of Directors

|  |

| |||

PROPOSAL 2: Advisory Vote to Approve the Company’s Executive Compensation for

| |

| |||

PROPOSAL 3: Advisory Vote on the Frequency of Future Advisory Votes on the Company’s Executive Compensation At the annual meeting you will be asked to vote on whether future advisory votes on the company’s executive compensation should occur every year, every two years or every three years. The Board recommends voting “for” holding future advisory votes on the company’s executive compensation annually. |

| ||||

PROPOSAL

2023. | |

| |||

|

4

|

Board of Directors and Corporate Governance |

Corporate Governance

| Director Independence | ||

| Board Leadership Structure | ||

| Board Committees | ||

| Other Governance Matters | ||

|

5

|

Prologis Corporate Governance Tear Sheet

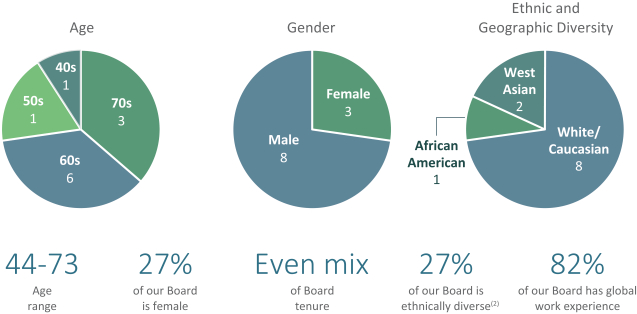

| DIRECTOR COMPOSITION AND EVALUATION PROCESS | |||

· 91% of our Board is independent: All directors, other than our chairman, are independent.

· No related-party transactions.

· No hedging or pledging of our securities.

· All directors attended 75% or more of Board and Board committee meetings.(1)

· All directors are in compliance with our stock ownership guidelines (5x annual cash retainer). | ||||

| · Annual Board evaluation process involving Board, Board committee and individual director assessments: Administered by the chair of our Board Governance and Nomination Committee (the “Governance Committee”) and our lead independent director, with a third-party evaluation every other year.

· Age/tenure policy: 75 years maximum age limit and 15-year maximum tenure limit.

· Our mix of director tenure, skills and background provides a balance of experience and institutional knowledge with fresh perspectives.

· Three directors are female, and three are ethnically diverse. | |||

| BOARD LEADERSHIP · Lead independent director role with significant authority and responsibilities.

· Chairman and CEO policy gives Board flexibility to determine best candidate for the positions. | |||

| STRONG STOCKHOLDER RIGHTS · All directors elected annually since IPO. Irrevocably opted out of Maryland staggered board provisions in 2014. · Adopted proxy access with 3/3/20/20 market standard

· No stockholder rights plan.

·

· Stockholders can amend bylaws with majority vote (adopted in 1997). | |||

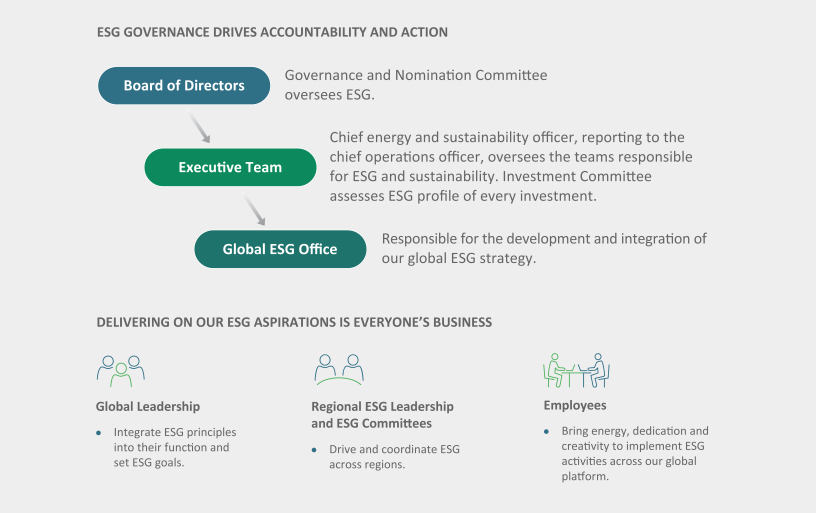

ESG GOVERNANCE · Formal board oversight over ESG efforts through Board Governance and Nomination Committee charter and updates to the full Board and other committees. · Energy, Sustainability, Mobility and ESG group reporting directly to C-suite (COO). · Accountability structure and ESG bonus metrics to incentivize success of ESG. | RISK GOVERNANCE · Financial risk oversight: Evidenced by A3/A credit ratings.(4) · Operational risk oversight: Annual enterprise level risk analyses with board; climate risk assessment platform; rigorous investment committee processes; local team property-level management. · Reputational risk oversight: Extensive employee learning and development platform requiring ethics, cybersecurity, diversity and other training. | |||

| (1) | Mr. Connor, who was appointed to the Board in October 2022, attended all Board meetings subsequent to his appointment. |

Our governance guidelines provide that directors will not be nominated or appointed to the Board if they are, or would be, 75 years or older or with 15 or more years of board tenure at the time of the election or appointment. Our board tenure policy applies to any director newly appointed or elected after the tenure policy was implemented (for purposes of calculating tenure limits, tenure of the directors incumbent as of the day of policy adoption started on the date of adoption). |

|

See “Additional Information” for further detail on proxy access. |

| (4) | Ratings by Moody’s/S&P. A securities rating is not a recommendation to buy, sell or hold securities and is subject to withdrawal at any time by the rating agency. |

|

6

|

Election of Directors (Proposal 1)

· The eleven nominees for election to the Board at the 2023 annual meeting, all proposed by the Board, are listed below in the section titled “Director Nominees,” along with brief biographies. · The Board has affirmatively determined that all of our director nominees, other than Hamid Moghadam, are independent directors in accordance with New York Stock Exchange (“NYSE”) rules, our governance guidelines and our bylaws.

·

· Information about each director nominee’s share ownership is presented below under “Security Ownership.”

The shares represented by the proxies received will be voted for the election of each of the eleven nominees named below, unless you indicate in the proxy that your vote should be cast against any or all of the director nominees or that you abstain from voting. Each nominee elected as a director will continue in office until his or her successor has been duly elected and qualified, or until the earliest of his or her resignation, retirement or death.

|

The Board unanimously recommends that the stockholders vote FOR the

election of each nominee.

|

7

|

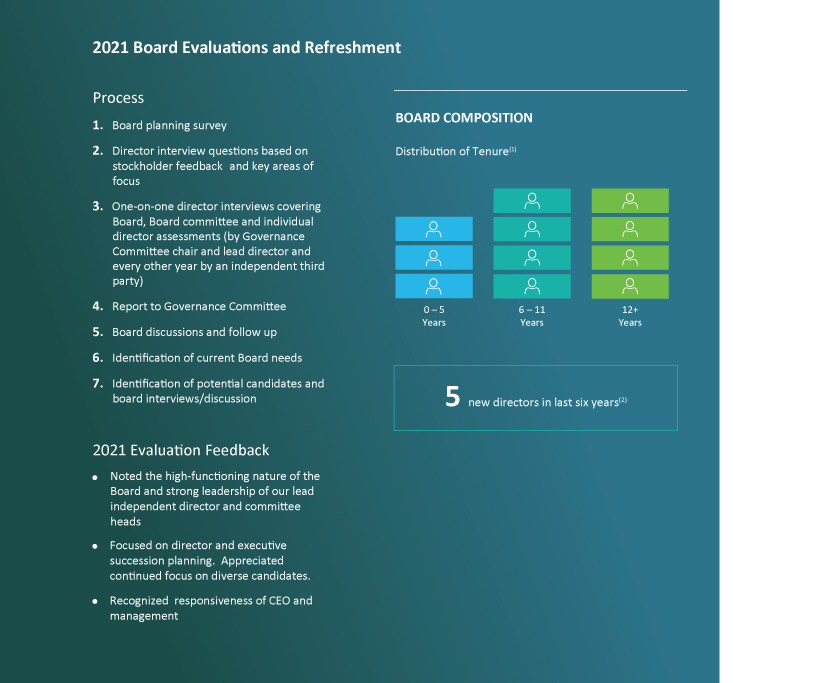

HOW IT WORKSBoard Evaluations and Process For Selecting Directors

Rigorous Board evaluation and refreshment process

Our annual Board evaluation process involves assessments at the Board, Board committee and individual director levels. Through this process, the Board determines who should be nominated to stand for election based on current company and Board needs. · Directors identify key skills and characteristics currently needed for the Board, as well as to provide information relating to Board composition and planning. · Director interview questions are prepared based on current areas of focus as well as feedback from our stockholder outreach efforts. · Annual one-on-one director interviews are conducted by our lead independent director and chair of the Governance Committee and, every other year, by an independent third party. · The results of the director interviews are aggregated by our lead independent director, Governance Committee chair, and if applicable, the independent third party, and reported to the Governance Committee and then to our full Board. Our Board follows up on items identified in the evaluation process. Our Governance Committee discusses Board succession and reviews potential candidates. This process is based on the results of annual board evaluations and takes place throughout the course of the year. · Our director candidate search process actively identifies and assesses a pool of potential candidates through a variety of sources, primarily through internal references. Although the committee may retain third parties to assist in identifying potential nominees, it prefers internal references by directors who understand the needs and dynamics of the Board with a particular focus on inclusion and diversity of ideas and background. · In 2021, we implemented a director/CEO recruitment diversity policy that requires the Governance Committee to consider (and any staffing agencies to recruit) ethnic and gender diverse candidates in formal director searches and recruitment for external CEO candidates. · Our governance guidelines also ensure regular board refreshment, providing that directors will not be nominated or appointed to the Board if they are, or would be, 75 years or older or with 15 or more years of board tenure at the time of the election or appointment. |

2023 Board evaluation feedback

Key feedback from our Board evaluation process:

· Noted the high-functioning nature of the Board and strong leadership of our lead independent director and committee heads. · Focused on executive succession planning. · Also focused on director succession planning and an orderly transition of key leadership positions and directors with institutional knowledge (coordinated with executive succession planning). · Recognized the strength of our CEO and management. · Determined that there were no concerns about Board independence or longer tenured directors. |

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 8 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

Regular Board refreshment

The Board is committed to regular refreshment to maintain an optimal balance of different perspectives, skills and backgrounds. We have onboarded six new directors in the past eight years, increasing the ethnic, gender and geographical diversity of the Board as well as breadth of experience. As a priority, the Board continues to be particularly focused on ethnic and gender diverse candidates who meet the current needs of the company.

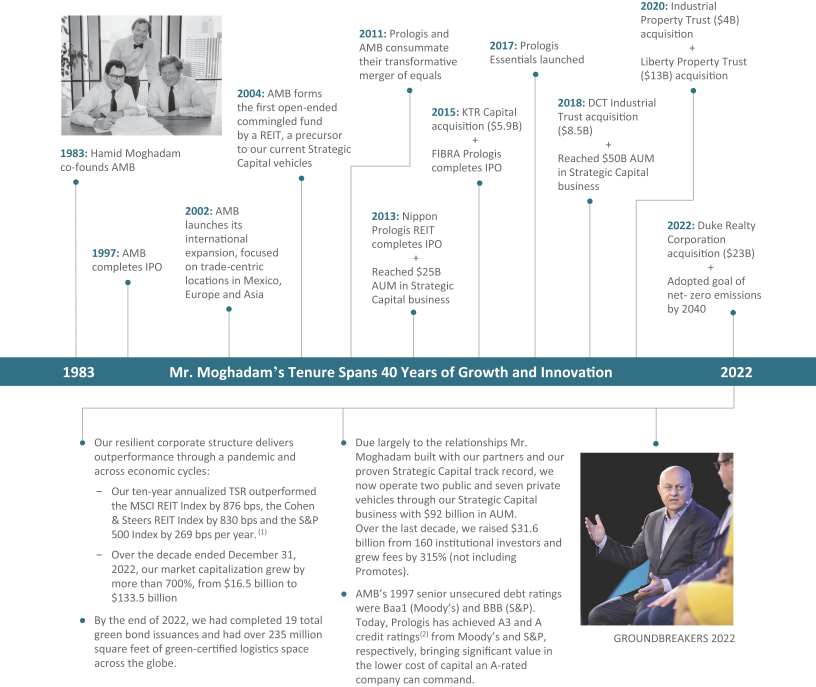

The Board was completely refreshed and rebuilt at the time of the Merger(2) in 2011. The Merger essentially created a new company with a new operating and corporate platform. At that time, all directors underwent intensive review to determine which directors would best fit the newly created combined company. Each director selected in this rebuilding process was onboarded as a new director to the newly established company. These directors were required to perform in a new governance environment, with new structures, processes, committees, charters and guidelines.

We have continued to refresh the Board since the Merger. David O’Connor onboarded as a new director in 2015, Olivier Piani in 2017, Cristina Bita and Philip Hawkins in 2018, Avid Modjtabai in 2020 and James Connor in 2022. (In 2020, Mr. Hawkins took a position as executive chairman of a U.S. industrial real estate portfolio company and, as a result, decided to step down from our Board).

As a result of our regular board refreshment, the Board comprises an appropriate mix of tenures: four directors with up to six years of tenure, three directors with tenure between six and twelve years and four with over twelve years of tenure. This mix provides an even balance of experience and institutional knowledge with fresh perspectives.

The Board is focused on director succession planning as a priority. As directors approach the maximum age and/or tenure limit set forth in our director age and tenure policy, the Board proactively formulates a plan to transition key leadership positions and maintain the appropriate balance of institutional knowledge on the Board. As discussed in “Board Qualifications,” the Board continually assesses the current needs of the Board based on the strategic priorities of the company and actively recruits candidates with a focus on the diversity and skill set needs of the Board.

EVEN DISTRIBUTION OF DIRECTOR TENURE(1)(2)

6 | new directors in last eight years.(3) | |

| (1) | Directors nominated for election at our 2023 annual meeting of shareholders. |

| (2) | The entire Board was rebuilt in 2011 at the time of the merger (the “Merger”) between AMB Property Corporation and ProLogis (the “Trust”) and the tenure of the rebuilt Board started at that time. However, we include Mr. Moghadam, Ms. Kennard, Mr. Webb and Mr. Skelton in the 12+ year category as they were directors of the legal acquirer prior to the Merger. |

Includes Philip Hawkins, who joined our Board in 2018 and stepped down from our Board in 2020 to assume an executive chairman position at a U.S. industrial real estate company. |

|

|

Director skills and experience support our business strategy

We have deep experience on our Board Evaluationscovering all components of our business model. The Board believes a balance of perspectives from other industries is critical to well-rounded oversight and Process for Selecting Directorsinsight into our customers’ perspectives.

Rigorous board evaluation and refreshment process

BUSINESS STRATEGY | DIRECTOR EXPERIENCE | FINANCIAL RESULTS(1) | ||||||

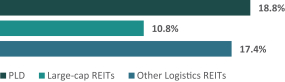

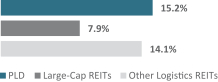

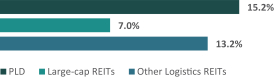

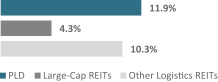

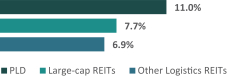

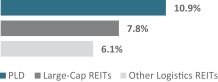

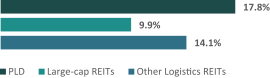

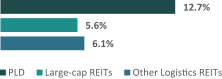

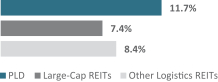

Global presencein the heart | 82% of our directors have global | Strong long-term performance 23.4% earnings per share CAGR and 11.7% Core FFO per share CAGR,(2) 1,566 bps and 428 bps above the Large-Cap REIT Group average | ||||||

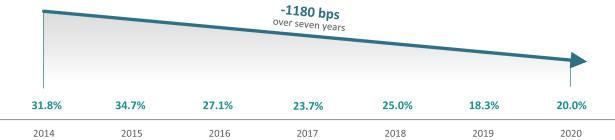

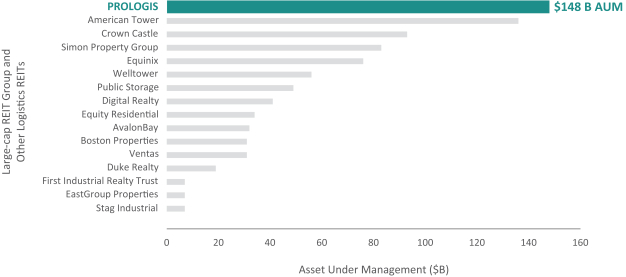

Scaledrives efficiency | 100% of our directors have large | Significant and durable growth 306% AUM growth while G&A(3) as a percentage of AUMdecreased | ||||||

Developmentenhances the bottom line | 55% of our directors have real | Building an irreplaceable portfolio $7.9B in value created by our development business(4) | ||||||

Strategic Capitalboosts | 100% of our directors have investment | A high return business $4.1B delivered in strategic capital fees and Promotes | ||||||

Essentials, our platform offering logistics solutions, services and products, provides new revenue streams and strengthens customer relationships | 36% of our directors have experience with customer products, services and solutions | Additional earnings opportunities Total Essentials contracted sales grew by 150% from 2021 to 2022 | ||||||

| (1) |

|

| (2) |

|

|

|

|

|

|

|

|

Regular Board refreshment

|

|

|

|

|

|

|

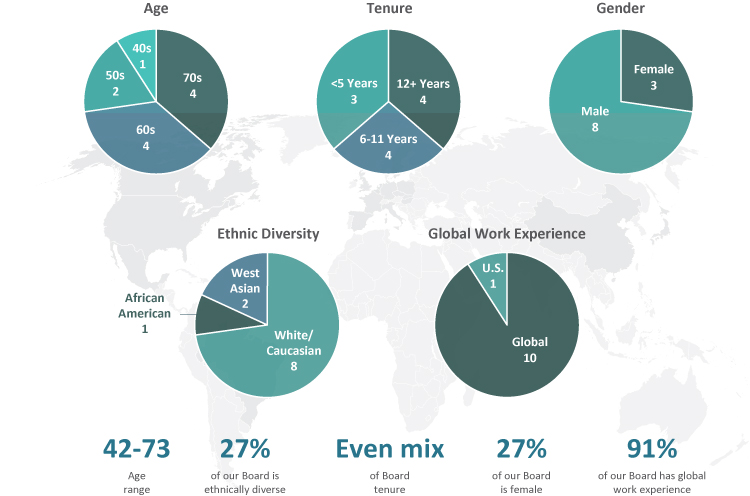

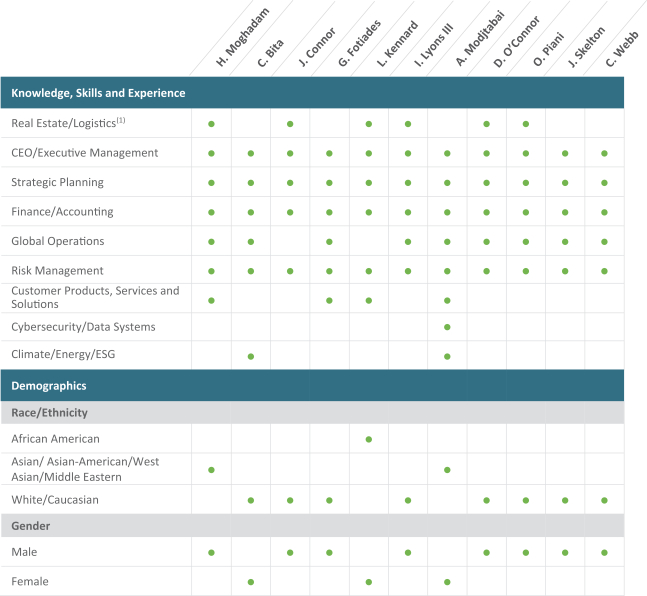

Director Qualifications, Skills and Experience

Board composition and diversity

|

|

|

|

PROLOGIS BOARD DIVERSITY

|

|

Board Qualifications

Director skills and experience support our business strategy.

|

|

Our global platform outperformed the average of the |

| (3) | “G&A” are our general and administrative expenses. |

| (4) | Value created over our total expected investment through development and leasing activities based on current projections. Please see Appendix A for further detail regarding how we calculate “Value creation.” Development value creation is calculated across our owned and managed portfolio. |

|

|

Board composition and diversity

Our board diversity policy centers on our commitment to maintaining Board diversity in thought, background and experience—a mix of gender, ethnic background, geographic origin and professional experience that supports our business strategy and the current needs of the Board. As such, the Governance Committee focuses on identifying and nominating qualified and diverse director candidates with commensurate experience and background and each of our director nominees was chosen on this basis.

Our directors nominated for election at our 2023 annual meeting support this mix of diversity in gender, ethnicity and background (see the director demographics/skills matrix below). We are continually seeking new, diverse candidates to add to our Board—our current pipeline of potential candidates is comprised of mostly diverse individuals. Our board diversity policy (which is published on our website in our Governance Guidelines) requires that in any formal search for new directors, the Board will consider, and will instruct any third-party search firm to include, candidates from diverse backgrounds, including in its initial list both gender and racial/ethnic diverse director candidates.

In making its nominations, the Governance Committee also assesses each director nominee by key characteristics, including courage to voice opinions, integrity, experience, accountability, good judgment, supportiveness in working with others and willingness to commit the time needed to satisfy the requirements of Board and committee membership.

PROLOGIS BOARD DIVERSITY(1)

| (1) |

|

| (2) |

|

|

|

|

Director skills and experience support our business strategy

We have deep experience on our Board covering all components of our business model. The Board believes a balance of perspectives from other industries is critical to well-rounded oversight and insight into the perspectives of our customers covering a wide range of industries.

Along with the fundamental characteristics necessary for all directors, such as courage, wisdom and good judgment, below are qualifications of our Board identified in our Board evaluation process as important to support our current business strategy. These characteristics, coupled with diversity of thought and background, are critical to strong oversight and proven long-term results.

We also seek directors with skillsets that support our emerging areas of focus, including cybersecurity, data and energy. We consider whether candidates possess experience in such areas when evaluating potential directors.

| (1) | Includes development, operations, real estate investments and fund management. |

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 12 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

Director Nominees

Hamid R. Moghadam

| Hamid R. Moghadam · Chairman of the Board since January 2000; Director since November 1997

· Board Committees: Executive

· Other public directorships: None |

Mr. Moghadam, 64,66, has been our Chief Executive Officerchief executive officer since the end of December 2012 and was our Co-Chief Executive Officerco-chief executive officer from June 2011 to December 2012. He is the co-founder of AMB Property Corporation and was AMB’s Chief Executive Officerchief executive officer from November 1997 (from the time of AMB’s initial public offering) to the Merger in June 2011 when AMB merged with the Trust.2011.

Other relevant qualifications.qualifications: Mr. Moghadam is on the board of the Stanford Management Company and formerly served as its chairman. He is a former trustee of Stanford University and previously served on the Executive Committee of the Board of Directors of the Urban Land Institute. Mr. Moghadam holds Bachelor’s and Master’s degrees in engineering from the Massachusetts Institute of Technology and a Master of Business Administration from the Graduate School of Business at Stanford University.

Irving F. Lyons IIISkills related to company opportunities and risks: Mr. Moghadam co-founded our company 40 years ago. He brings unique value as a founder who has built an unparalleled platform that has consistently outperformed both the REIT industry and S&P 500. Mr. Moghadam has unmatched experience running the largest publicly traded industrial REIT in the world with real estate operations and development across 19 countries. Mr. Moghadam built our Strategic Capital business (including two public companies and seven private vehicles), which is unrivaled in the REIT industry. His vision has further positioned the company for growth by creating an ecosystem of products, services and solutions for our customers via our Essentials platform. See page 55 for more information regarding Mr. Moghadam’s exceptional contributions to Prologis over the past four decades.

| Irving F. Lyons III · Lead independent director since June 2011 (prior to the Merger served as a trustee of the Trust from September 2009 to June 2011 and from March 1996 to May 2006)

· Board Committees: Executive

· Other public directorships: Equinix, Inc. and Essex Property Trust, Inc. |

Mr. Lyons, 71,73, has been a principal with Lyons Asset Management, a private equity firm, since January 2005. In 2004, Mr. Lyons retired from the Trust where he served as chief investment officer from 1997 until his retirement. He joined the Trust in 1993 and served as president from 1999 to 2001 and vice chairman from 2001 to 2004. Mr. Lyons is a member of the boards of Equinix, Inc., a global data center operator, and Essex Property Trust, Inc., a real estate investment trust investingthat invests in apartment communities. Mr. Lyons previously served as chairman of the board of BRE Properties, Inc.

Other relevant qualifications.qualifications: Mr. Lyons joined the Trust when King & Lyons, an industrial real estate management and development company, was acquired by the Trust in 1993. Mr. Lyons had been the managing general partner in that firm since its inception in 1979 and was one of its principals at the time of the acquisition. Mr. Lyons holds a Master in Business Administration from Stanford University and a Bachelor of Science in industrial engineering and operations research from the University of California at Berkeley.

Skills related to company opportunities and risks: Mr. Lyons’ service as an executive in the logistics real estate industry, including as chief investment officer and president of the Trust, as a principal of a private equity firm and in leadership roles on the boards of other publicly traded REITs guide his oversight as our Board’s lead independent director.

|

|

Cristina G. Bita

| Cristina G. Bita · Director since May 2018

· Board Committees: Audit

· Other public directorships: None |

Ms. Bita, 42,44, is a Vice Presidentvice president of Financefinance at Google and Business Finance Officerserves as the business finance officer for Google’s Devices and Services product area, Googleand Global Marketing organization and Google Sustainability. Sheorganizations. Ms. Bita leads global finance activities for consumer hardware, consumer paid services as well as for the company’s marketing investments globally. Ms. Bita has served in a number ofheld several finance leadership roles since joiningover the course of her 15+ year career at Google in 2006 across a range of business areas, including Global Partnershipsthat also included Sales and Business Development, Global Sales, and Consumer Products, Platforms and Platforms.Ecosystems, G&A, and Technical Infrastructure and Enterprise. She has also served as the chair of the Google Sustainability Board. Prior to Google, Ms. Bita spent six years with Siemens/Osram, where she held various positions at Siemens/Osram in the Business Unit Controllership and Corporate FP&A.&A groups.

Other relevant qualifications.qualifications: Ms. Bita holds a Master of Science in Finance from the Boston College Wallace E. Carroll School of Management and a Bachelor of Science in Business Administration (Accounting) from Salem State University. Ms. Bita is also a Certified Management Accountant (CMA).

George L. FotiadesSkills related to company opportunities and risks: Ms. Bita’s experience in innovation and technology gained from her tenure at Google supports our strategic initiatives to stay ahead of the evolution of the supply chain and our customers’ needs by integrating data systems and technology across both our core real estate and Essentials platforms. Ms. Bita also served as the chair of the Google Sustainability Board, which provides valuable insights in support of our ESG initiatives.

| James B. Connor · Director since October 2022 · Board Committees: Executive · Other public directorships: EPR Properties and Healthpeak Properties, Inc. |

Mr. Connor, 64, was most recently chairman and chief executive officer of Duke Realty Corporation, a NYSE-listed company that specialized in modern, bulk warehouse and logistics facilities and was acquired by Prologis in October 2022. Mr. Connor joined Duke Realty in 1998 and served in several leadership positions before being named CEO in 2016. Before joining Duke Realty, Mr. Connor held numerous executive and brokerage positions with Cushman & Wakefield. Additionally, Mr. Connor is a member of the board of trustees of EPR Properties, a publicly traded REIT focused on real estate venues that facilitate out of home leisure and recreation experiences and the board of directors of Healthpeak Properties, Inc., a publicly traded REIT focused on real estate related to the healthcare industry.

Other relevant qualifications: Mr. Connor is a member of the Executive Board of Governors of the National Association of Real Estate Investment Trusts (Nareit). Mr. Connor holds a Bachelor of Business Administration degree with a minor in Real Estate Finance from Western Illinois University.

Skills related to company opportunities and risks: Mr. Connor brings over a quarter century of experience in the logistics REIT industry, including seven years as a public company CEO. His deep experience guides all aspects of our business related to the logistics real estate industry.

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 14 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

| George L. Fotiades · Director since June 2011 (prior to the Merger served as a trustee of the Trust from December 2001 to June 2011)

· Board Committees: Compensation (Chair)

· Other public directorships: AptarGroup, Inc. |

Mr. Fotiades, 67, was appointed President69, served as president and Chief Executive Officer*chief executive officer of Cantel Medical Corp., a provider of infection prevention and control products, from 2019 until his retirement in March 2019.2021. Mr. Fotiades was an operating partner at Five Arrows Capital Partners (Rothschild Merchant Banking) from April 2017 until March 2019. From April 2007 to April 2017, Mr. Fotiades was a partner, healthcare investments at Diamond Castle Holdings LLP, a private equity firm. Mr. Fotiades was chairman of Catalent Pharma Solutions, Inc., a provider of advanced technologies for pharmaceutical, biotechnology and consumer health companies, from June 2007 to February 2010. Mr. Fotiades is Chairmanchairman of the board of AptarGroup, Inc., a global dispensing systems company and is also a director of Cantel Medical Corp.company. He previously served on the boardboards of Cantel Medical Corp. and Alberto-Culver Company, a consumer products company specializing in hair and skin careskincare products.

Other relevant qualifications.qualifications: Mr. Fotiades was previously the president and chief operating officer of Cardinal Health, Inc. and also served as president and chief executive officer of Cardinal’s Pharmaceutical Technologies and Services segment. Mr. Fotiades also served as president of Warner-Lambert’s consumer healthcare business, as well as in other senior positions at Bristol-Myers Squibb, Wyeth, and Procter & Gamble. Mr. Fotiades holds a Master of Management from The Kellogg School of Management at Northwestern University and a Bachelor of Arts from Amherst College.

* Skills related to company opportunities and risks: Mr. Fotiades will no longer bebrings experience as a public company CEO who ran large scale global operations as well as years of Cantel Medical Corp. (or CEO in any other capacity) upon the closing of Steris Corporation’s acquisition of Cantel Medical Corp., expected to occurexperience in the second quarter of 2021. Should the Steris acquisition terminate or not close, private equity industry.Mr. Fotiades will nevertheless retireFotiades’ experience at various consumer products and services companies adds valuable insights as CEO of Cantel Medical Corp.

|

|

Lydia H. Kennardwe continue to grow our Essentials business.

| Lydia H. Kennard · Director since August 2004

· Board Committees: Governance

· Other public directorships: Freeport-McMoRan Copper & Gold Inc., |

Ms. Kennard, 66,68, is the founder and chief executive officer of KDG Construction Consulting, a provider of project and construction management services, a principal of KDG Aviation, an aviation focused real estate operating and development company, the owner of KDG Holdings, Inc., parent of Quality Engineering Solutions, Inc., a pavement management analytics and construction inspection company, and a principal with 1031 N. Brand Boulevard, Glendale, LLC, aand 690 N. 2nd Street, Reno, LLC, both single-purpose real estate entity.entities. Ms. Kennard is a member of the boards of Freeport-McMoRan Copper & Gold Inc., a natural resource company, Healthpeak Properties, Inc., a healthcare real estate investment trust, and AECOM, an infrastructure consulting firm.firm, and Vulcan Materials Company, a leading producer of construction aggregates. Ms. Kennard was previously a member of the boards of URS Corporation, a provider of engineering, construction and technical services, and Intermec, Inc., an automated identification and data collection company.

Other relevant qualifications.qualifications: Ms. Kennard served as Chief Executive Officerchief executive officer of Los Angeles World Airports, a system of airports comprising Los Angeles International, Ontario International Airport, Palmdale Regional and Van Nuys General Aviation Airports from 1999 to 2003 and again from 2005 to 2007. From 1994 to 1999, she served as the system’s deputy executive for design and construction. Ms. Kennard holds a Juris Doctor degree from Harvard University, a Master’s degree in city planning from the Massachusetts Institute of Technology, and a Bachelor of Science in urban planning and management from Stanford University.

Avid ModjtabaiSkills related to company opportunities and risks: Ms. Kennard’s deep experience in the construction industry and urban planning supports our robust development platform. Ms. Kennard’s background as CEO of Los Angeles World Airports guides our efforts to grow our global logistics real estate business. As the owner of a construction analytics and solutions company, Ms. Kennard also provides experience in customer services and solutions.

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 15 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

| Avid Modjtabai · Director since February 2020

· Board Committees: Audit · Other public directorships: Avnet, Inc. |

Ms. Modjtabai, 59,61, served as the Senior Executive Vice Presidentsenior executive vice president and head of the Payments, Virtual Solutions and Innovation Group at Wells Fargo from 2016 to her retirement in March 2020. Prior to that, she served in various leadership roles at Wells Fargo, including Groupgroup head for Wells Fargo Consumer Lending from 2011 to 2016, Chief Information Officerchief information officer and head of Technology and Operations Group from 2008 to 2011, Chief Information Officerchief information officer and head of technology from 2007 to 2008, and Directordirector of Human Resourceshuman resources from 2005 to 2007. Ms. Modjtabai is a member of the board of Avnet, Inc., a global technology solutions provider.

Other relevant qualifications.qualifications: Ms. Modjtabai holds a Master in Business Administration in finance from Columbia University and a Bachelor of Science in industrial engineering from Stanford University.

|

|

David P. O’ConnorSkills related to company opportunities and risks: As the former chief information officer and head of technology of Wells Fargo, Ms. Modjtabai brings her experience overseeing core technology functions to our board. Ms. Modjtabai’s knowledge and skill in these areas supports the company’s own data and technology initiatives as well as our cybersecurity program. Ms. Modjtabai’s tenure as head of Payments, Virtual Solutions and Innovation at Wells Fargo brings additional customer solutions experience to our board.

| David P. O’Connor · Director since January 2015

· Board Committees: Compensation

· Other public directorships: Regency Centers Corporation |

Mr. O’Connor, 56,58, is a private investor, managing partner of High Rise Capital Partners, LLC, a private real estate investment firm, and a non-executive co-chairman of HighBrook Investors LLC. He was the co-founder and senior managing partner of High Rise Capital Management LP, a real estate securities hedge fund manager that operated from 2001 to 2011. Mr. O’Connor is a member of the board of Regency Centers Corporation, a publicly traded real estate investment trust specializing in shopping centers. He previously served on the boardboards of Songbird Estates plc, the former majority owner of Canary Wharf in London, UK and Paramount Group, Inc., a publicly traded real estate investment and management company specializing in office buildings.

Other relevant qualifications.qualifications: Mr. O’Connor was previously a principal, co-portfolio manager and investment committee member of European Investors, Inc., a large dedicated real estate investment trust investor, from 1994 to 2000. Mr. O’Connor received a Master of Science in real estate from New York University and holds a Bachelor of Science degree from the Boston College Wallace E. Carroll School of Management.

Olivier PianiSkills related to company opportunities and risks: Mr. O’Connor brings extensive knowledge in real estate investment to our Board, which supports all aspects of our global real estate operations, Strategic Capital business and capital markets activity.

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 16 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

| Olivier Piani · Director since May 2017

· Board Committees: Audit

· Other public directorships: None |

Mr. Piani, 67,69, is the chief executive officer and founder of OP Conseils, a consulting company in real estate and finance that Mr. Piani started in January 2016. Mr. Piani is also a senior consultant with Ardian, a major European private equity group. From September 2008 to December 2015, Mr. Piani was chief executive officer of Allianz Real Estate, the real estate and asset management investment platform for the Allianz Group.

Other relevant qualifications.qualifications: From 1998 to 2008, Mr. Piani built the pan-European platform for GE Capital Real Estate spanning seven different countries. Prior to joining GE in 1998, Mr. Piani was chief executive officer of UIC-Sofal, a real estate bank. From 1982 to 1995, Mr. Piani held various leadership positions in the Paribas Group in Paris, New York and London. Mr. Piani is a graduate of Paris Ecole Superieure de Commerce de Paris and received a Master of Business Administration from Stanford University.

|

|

Jeffrey L. SkeltonSkills related to company opportunities and risks: Mr. Piani’s experience in real estate and finance gained through his career in private equity, asset management and banking supports our long-term investment strategy and our Strategic Capital business. Mr. Piani’s financial expertise and deep knowledge of the European real estate market guides our operations and growth in that region as well as our expansion into new markets.

| Jeffrey L. Skelton · Director since November 1997

· Board Committees: Governance (Chair), Executive (Chair)

· Other public directorships: None |

Mr. Skelton, 71,73, retired in 2009 as president and chief executive officer of Symphony Asset Management, a subsidiary of Nuveen Investments, Inc., an investment management firm. After his retirement in 2009 and until 2013, Mr. Skelton was a co-founderco-founded and served as managing partner of Resultant Capital Partners, an investment management firm.

Other relevant qualifications.qualifications: Prior to founding Symphony Asset Management in 1994, Mr. Skelton was with Wells Fargo Nikko Investment Advisors from 1984 to 1993, where he served in a variety of capacities, including chief research officer, vice chairman, co-chief investment officer and chief executive officer of Wells Fargo Nikko Investment Advisors Limited in London. Previously, Mr. Skelton was also an assistant professor of finance at the University of California at Berkeley, Walter A. Haas School of Business. Mr. Skelton holds a Ph.D. in mathematical economics and finance and a Master of Business Administration from the University of Chicago.

Carl B. WebbSkills related to company opportunities and risks: Mr. Skelton’s significant leadership experience in the asset management industry supports our Strategic Capital business and forms a strong foundation for his oversight responsibilities as chair of our Governance and Executive Committees.

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 17 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

| Carl B. Webb · Director since August 2007

· Board Committees: Audit (Chair)

· Other public directorships: Hilltop Holdings Inc. |

Mr. Webb, 71,73, is currently a co-managing member of Ford Financial Fund II, L.P. and Ford Financial Fund III, L.P., private equity firms focusing on equity investments in financial services, a position he has held since February 2012 and March 2019, respectively. Mr. Webb has served as chairman of the Mechanics Bank board since April 2015. From June 2008 until December 2012, Mr. Webb was a senior partner of Ford Management, L.P. Mr. Webb was also the chief executive officer and a board member of Pacific Capital Bancorp and chairman of Santa Barbara Bank and Trust from August 2010 until December 2012. Mr. Webb has also served as a consultant to Hunter’s Glen/Ford, Ltd., a private investment partnership, since November 2002. Additionally, Mr. Webb is a member of the board of Hilltop Holdings Inc., a publicly traded financial services holding company.

Other relevant qualifications.qualifications: Mr. Webb previously served on the boards of Plum Creek Timber Company, M & F Worldwide Corp. and Triad Financial SM LLC, where he was co-chairman from July 2007 to October 2009 and served as interim president and chief executive officer from August 2005 to June 2007. Since 1983, Mr. Webb held executive positions at banking institutions, including Golden State Bancorp, Inc. and its subsidiary, California Federal Bank, FSB, First Madison Bank, FSB, First Gibraltar Bank, FSB and First National Bank at Lubbock. Mr. Webb holds a Bachelor of Business Administration from West Texas A&M University and a graduate banking degree from Southwestern Graduate School of Banking at Southern Methodist University.

Skills related to company opportunities and risks: Mr. Webb’s extensive finance experience gained over his career in private equity and banking supports our Strategic Capital business and his financial oversight role as chair of our Audit Committee.

|

18

|

William D. Zollars

|

|

Mr. Zollars, 73, retired from YRC Worldwide, Inc., a global transportation service provider, in July 2011 where he served as chairman, president, and chief executive officer from 1999 until his retirement. He was president of Yellow Transportation, Inc. from 1996 to 1999. Mr. Zollars is a member of the board of Cerner Corporation, a supplier of healthcare information technology solutions, healthcare devices and related services. Mr. Zollars also serves on the U.S. Postal Service Board of Governors. He is a former director of CIGNA Corporation, a global health service organization.

Other relevant qualifications. Mr. Zollars was previously a senior vice president of Ryder Integrated Logistics, a division of Ryder System, Inc. and he spent 24 years in various executive positions, including eight years in international locations, at Eastman Kodak. Mr. Zollars holds a Bachelor of Arts in economics from the University of Minnesota.

|

|

We require that a majority of the Board be independent in accordance with NYSE rules. To determine whether a director is independent, the Board must affirmatively determine that there is no direct or indirect material relationship between the company and the director.

91% of the Board is independent.(1)

The Board has determined that all our directors, with the exception of our chairman, Mr. Moghadam, are independent.

|

The Board reached this determination after considering all relevant facts and circumstances, reviewing director questionnaires and considering transactions and relationships, if any, between us, our affiliates, our executive officers and their affiliates, and each of the directors, members of each of their immediate families and their affiliates.

Audit, Governance and Talent and Compensation Committees are 100% independent.

The Board has also determined that all members of the Audit, Governance and Talent and Compensation Committees of the Board are independent in accordance with NYSE and Securities and Exchange Commission (“SEC”) rules.

|

Our governance guidelines do not specify a leadership structure for the Board, allowing the Board the flexibility to choose the best option for the company as circumstances warrant. The Board believes that strong independent leadership ensures effective oversight over the company. Such independent oversight is maintained through:

| · | our lead independent director; |

| · | our independent directors; |

| · | the Audit, Governance and Talent and Compensation Committees, which are all comprised entirely of independent directors; |

| · | annual review of the Board leadership structure and effectiveness of oversight through the Board evaluation process; and |

| · | strong adherence to our governance guidelines. |

All of our independent directors have the ability to provide input for meeting agendas and are encouraged to raise topics for discussion by the Board. In addition, the Board and each Board committee has complete and open access to any member of management.

Each committee has the authority to retain independent legal, financial and other advisors as they deem appropriate without consulting or obtaining the approval of any member of management. The Board also holds regularly scheduled executive sessions of only independent directors in order to promote free and open discussion among the independent directors.

|

|

Chairman and CEO assessment

Our chairman and CEO and our lead independent director act together in a system of checks and balances, providing both strong oversight and operational insight.

Our CEO, Mr. Moghadam, serves as chairman of the Board. The lead independent director role is focused on ensuring independent oversight of the company. Mr. Moghadam’s roles as both CEO and chairman enable him to act as a bridge between management and the Board, ensuring that the Board understands our business when making its decisions.

| (1) | Directors nominated for election at our 2023 annual meeting of shareholders. |

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 19 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

Mr. Moghadam has the breadth of experience to execute our unique business plan and to provide special insights to the Board.

Very few have experience running a public company with extensive global real estate operations and substantial strategic capitalStrategic Capital and development businesses. Mr. Moghadam co-founded the company and has served on the Board since the company’s initial public offering in November 1997. As one of our founders, Mr. Moghadam has extensive knowledge and expertise in the real estate and REIT industries, as well as history and knowledge of our company.

Considering all of these factors, the Board believes that a structure that combines the roles of CEO and chairman, along with an independent lead director, independent chairs for each of the Board committees and independent non-employee directors, provides the best leadership for the company at this time and places the company in a competitive position to provide long-term value to our stockholders. Through its annual board evaluation process (led by an independent third-party evaluator every other year), the board regularly assesses this structure and determines whether it continues to be in the best interests of the company and its stockholders.

Lead independent director

If the offices of chairman and CEO are held by the same person or if the chairman is otherwise not independent, the independent members of the Board will annually elect an independent director to serve in a lead capacity. The lead independent director is generally expected to serve for more than one year. Mr. Lyons has been selected as the lead independent director by our Governance Committee and the independent members of our Board and has served in that capacity for nearly ten years.Board.

The lead independent director coordinates the activities of the other independent directors and performs other duties and responsibilities as determined by the Board.

The specific responsibilities of the lead independent director are currently as follows:

Executive Sessions/ Committee Meetings | · Presides at all meetings of the Board at which the chairman is not present, including executive sessions of the independent directors (generally held at every regular Board meeting)

· Attends meetings of the various Board committees regularly

| ||

Meetings of Independent Directors | · Has the authority to call meetings of the independent directors and set the agenda | ||

Board Evaluations | · Oversees, with the chair of the Governance Committee and, when applicable, an independent | ||

and CEO |

| ||

| · Serves as liaison between the independent directors and the chairman

· Meets regularly between Board meetings with the chairman and CEO | ||

Board Processes and Information | · Ensures the quality, quantity, appropriateness and timeliness of information provided to the Board and provides input to create meeting agendas

· Ensures that feedback is properly communicated to the Board and chairman

· Ensures the institution of proper Board processes, including the number, frequency and scheduling of Board meetings and sufficient time for discussion of all agenda items | ||

Communications with Stockholders | · Responds to stockholder inquiries and communicates with stockholders when appropriate | ||

|

|

Pursuant to the Maryland General Corporation Law and our bylaws, our business, property and affairs are managed under the direction of the Board. Members of the Board are kept informed of our business through our executive management team.

The four standing committees of the Board are: Audit, Governance, Talent and Compensation (the “Compensation Committee”) and Executive Committee (the “Executive Committee”). The Board has determined that each member of the Audit, Governance and Talent and Compensation Committees is an independent director in accordance with NYSE and SEC rules.

The current membership information for our Board committees is presented below.

Each committee has a charter which generally states the purpose of the committee and outlines the committee’s structure and responsibilities. The committees, other than the Executive Committee, must review their charter on an annual basis.

PROLOGIS BOARD COMMITTEES

Audit Committee

Members: Carl Webb (Chair), Cristina Bita, Avid Modjtabai and Olivier Piani

Number of Meetings in 2020: 9

| Audit Committee |

Members: Carl Webb (Chair) Cristina Bita Avid Modjtabai Olivier Piani | Meetings in 2022: 9 | Independence: The Board has determined that all members of the Audit Committee are independent in accordance with NYSE and SEC rules. | ||||||

Role and Responsibilities:

| · | Oversees the financial accounting and reporting processes of the |

| · |

|

| · |

|

| · |

|

| · | Oversees company process for developing data systems and disclosures related to emerging climate disclosure regimes. |

| · | All committee members are designated by the Board as “audit committee financial experts” in accordance with SEC regulations and meet the independence, experience and financial literacy requirements of the NYSE and Section 10A of the Securities Exchange Act of 1934, as |

| Talent and Compensation Committee |

Members: George Fotiades (Chair) David O’Connor William Zollars | Meetings in 2022: 5 | Independence: The Board has determined that all members of the Talent and Compensation Committee are independent in accordance with NYSE and Securities and Exchange Commission rules. | ||||||

Role and Compensation Committee

Members: George Fotiades (Chair), David O’Connor and William Zollars

Number of Meetings in 2020: 6Responsibilities:

| · |

|

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 21 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

| · | Approves and evaluates our director and officer compensation plans, policies and |

| · |

|

| · |

|

| · |

|

|

|

|

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

| Board Governance and Nomination Committee |

Members: Jeffrey Skelton (Chair) Lydia Kennard William Zollars | Meetings in 2022: 3 | Independence: The Board has determined that all members of the Governance Committee are independent in accordance with NYSE and SEC rules. | ||||||

Role and Nomination Committee

Members: Jeffrey Skelton (Chair), Lydia Kennard and William Zollars

Number of Meetings in 2020: 3Responsibilities:

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

Executive Committee

| · | Reviews company political lobbying activity and spending. |

Members: Jeffrey Skelton (Chair), Irving Lyons III and Hamid Moghadam

Number of Meetings in 2020: 0

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 22 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

| Executive Committee |

Members: Jeffrey Skelton (Chair) James Connor Irving Lyons III Hamid Moghadam | Meetings in 2022: None | Independence: The Board has determined that James Connor, Jeffrey Skelton and Irving Lyons III are independent in accordance with NYSE and SEC rules. | ||||||

Role and Responsibilities:

| · | Acts only if action by the Board is required, the Board is unavailable, and the matter is |

| · |

|

impose. |

|

Board’s role in risk oversight

Risk awareness is embedded throughout our operations, underpinned by an integrated framework for identifying, assessing and managing risk.

The Board has the primary responsibility for overseeing risk management of the company. Oversight for certain specific risks falls under the responsibilities of our Board committees.

| · | The Audit Committee focuses on financial and cybersecurity risks relating to the |

| · | The Talent and Compensation Committee focuses on risks relating to human capital management, talent retention and remuneration of our officers and |

| · | The Governance Committee focuses on reputational, corporate governance and ESG |

These committees regularly advise the full Board of their risk oversight activities.

Critical components of our risk oversight framework include regular communication among the Board, our management executive committee and our risk management infrastructure to identify, assess and manage risk.

Identifying, managing and assessing risks

|

|

Identifying, Managing and Assessing Risks

Our risk oversight framework includes:

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

| · |

|

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 23 |

Cybersecurity

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

Climate risk

We assess natural hazard and climate risk across our portfolio. Our Chief Technology Officerrisk management team works to ensure we have sufficient insurance coverage and protection for our buildings. We also partner with a global reinsurance company to evaluate future climate scenarios and determine which actions we should take. This evaluation is based on underwriting data, a significant improvement over the traditional catastrophe modeling and flood zone data used by many other organizations. Based on this evaluation, we take a range of actions which can include improving the physical resilience of our buildings, reviewing and improving disaster response plans, and other measures. Because of our long-term planning, resilience measures and diverse portfolio footprint, we believe our climate risk is well-managed.

Cybersecurity

Our chief technology officer and our Vice Presidentvice president of IT Governancegovernance oversee our information security program. They report to the audit committee/board at least annually and also conduct annual information security compliance training. The Prologis Information Security Policy is governed by the NIST Cybersecurity Framework (CSF) and includes mandatory annual training for all employees. Prologis’ cybersecurity posture is reviewed and benchmarked against its peers through regular participation in a third-party security benchmarking survey. Our IT infrastructure is externally audited as part of our Sarbanes Oxley audit process and our controls include information security standards. Also, we maintain standalone cybersecurity insurance. To our knowledge, we have not experienced a material breach in information security.

CEO and management succession planning

The Board is responsible for ensuring that we have a high-performing management team in place. The Board, with the assistance of the Talent and Compensation Committee, regularly conducts a detailed review of management development and succession planning activities to ensure that top management positions, including the CEO position, can be filled without undue interruption.

Our succession planning process is two-tiered to ensure orderly succession. One tier contemplates succession planning in the case of an emergency during which one or more members of our current management are unable to perform their duties. The second tier involves long-term planning to identify and develop talent with potential to step in as our future management team. As part of our longer termlonger-term succession planning, we made changes in 2019 and 2020 to our organizational architecture to prepare the company for the next chapter in its evolution. Executive roles were reorganized to drive our platform initiatives focusing on customer centricity and extracting value beyond our real estate while allowing for growth opportunities for the next generation of potential leaders. As an example, Mr. Olinger was instrumental in positioning his successor, Mr. Arndt, with key global leadership responsibilities to prepare Mr. Arndt for the role of CFO after Mr. Olinger’s retirement. Mr. Arndt assumed the position of CFO on April 1, 2022. Likewise, Mr. Reilly helped to prepare Mr. Letter for the role of president, which Mr. Letter assumed on January 1, 2023, through a variety of leadership roles at the company related to capital deployment and global operations. Also see “Compensation Committee Rationale: NEO Succession Planning” for a discussion of the committee’s approach regarding successor NEO compensation.

Communications with directors

We appreciate your input. Our lead independent director (or any of our other directors) are accessible to our stockholders and other interested parties for engagement as appropriate. You can communicate with any of the directors, individually or as a group, by writing to them in care of Edward S. Nekritz, Secretary, Prologis, Inc., Pier 1, Bay 1, San Francisco, California 94111. Each communication intended for the Board and received by the secretary that is related to the operation of the company and is not otherwise commercial in nature will be forwarded to the specified party following its clearance through normal security procedures. The directors will be advised of any communications that were excluded through normal security procedures as appropriate and they will be made available to any director who wishes to review them.

|

|

Director attendance

The Board held foureight meetings in 2020,2022, including telephonic meetings, and all of the directors attended 75% or more of the aggregate number of Board and applicable committee meetings on which he or she served during 20202022 (held during the periods they served). Each director standing for election in 20212023 is expected to attend the annual meeting of stockholders, either virtually or telephonically, absent cause. All of our directors attended the annual meeting last year, virtually or telephonically.telephonically, other than Mr. Connor who was appointed to the Board after the 2022 annual meeting.

Director compensation

Please see “Director Compensation” and the table titled “Director Compensation for Fiscal Year 2020.2022.”

Stock ownership guidelines and prohibition on hedging/pledging

Our directors must comply with our stock ownership guidelines which require the director to maintain an ownership level in our common stock equal to five times the annual cash retainer (a total of $600,000 as of December 31, 2020)2022). Shares included as owned by directors for purposes of the guidelines include common stock owned, vested or unvested equity awards (restricted stock, restricted stock units, shares and share units deferred under the terms of the Director Deferred Fee Plan or the applicable non-qualified deferred compensation plan, deferred share units and dividend equivalent units) and operating partnership or other partnership units exchangeable or redeemable for common stock. Until such time as the ownership thresholds are met, we will require directors to retain and hold 50% of any net shares of our common stock issued to our directors under our equity compensation plans.

Additionally, our insider trading policy prohibits our directors and employees from hedging the economic risk of ownership of our common stock and from pledging shares of our common stock.

All of our directors and executive officers are currently in compliance with the stock ownership guidelines and the prohibition on hedging and pledging our common stock.

Independent compensation consultant

The Talent and Compensation Committee directly engaged an outside compensation consulting firm, Frederic W. Cook & Co., Inc. (“FW Cook”)Pay Governance, to assist the committee in assessing our compensation programs for our Board, our CEO and other members of executive management. FW Cook reported directly to the Compensation Committee. FW Cook received no compensation from the company other than for its work in advising the Compensation Committee and maintained no other economic relationships with the company. FW Cook interacted directly with members of our management only on matters under the Compensation Committee’s oversight.

FW Cook conducted a comprehensive competitive review of the compensation program for our executive officers and our non-employee directors in April 2020, which was used by the Compensation Committee to assist it in making compensation recommendations to the Board. Our CEO makes separate recommendations to the Compensation Committee concerning the form and amount of the compensation of our executive officers (excluding his own compensation). FW Cook has also assisted the Compensation Committee in evaluating the design of certain outperformance compensation plans first implemented in 2012.

The Compensation Committee considered the independence of FW Cook in light of the rules regarding compensation committee advisor independence mandated under the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”). The Compensation Committee reviewed factors, facts and circumstances regarding compensation consultant independence, including a letter from FW Cook addressing FW Cook’s and their consulting team’s independent status with respect to the following factors: (i) other services provided to us by FW Cook; (ii) fees we pay to FW Cook as a

|

|

percentage of their total revenues; (iii) FW Cook’s policies and procedures that are designed to prevent conflicts of interest; (iv) any business or personal relationship between FW Cook or members of their consulting team that serves the Compensation Committee and a member of the Compensation Committee; (v) any shares of our stock owned by FW Cook or members of their consulting team that serves the Compensation Committee; and (vi) any business or personal relationships between our executive officers and FW Cook or members of their consulting team that serves the Compensation Committee. After discussing these factors, facts and circumstances, the Compensation Committee affirmed the independent status of FW Cook and concluded that there are no conflicts of interest with respect to FW Cook.

At the end of 2020, the Compensation Committee engaged another compensation consulting firm, Pay Governance, switching our compensation consulting firms as a good compensation governance practice. Pay Governance reports directly to the Talent and Compensation Committee. Pay Governance receives no compensation from the company other than for its work in advising the Talent and Compensation Committee and maintains no other economic relationships with the company. Pay Governance interacts directly with members of our management only on matters under the Talent and Compensation Committee’s oversight.

Pay Governance conducted a comprehensive competitive review of the compensation program for our non-employee directors in May 2022 and executive officers in December 2022, which was used by the Talent and Compensation Committee to assist it in making compensation recommendations to the Board. Our CEO makes separate recommendations to the Talent and Compensation Committee concerning the form and amount of the compensation of our executive officers (excluding his own compensation).

The Talent and Compensation Committee considered the independence of Pay Governance in light of the rules regarding compensation committee advisor independence mandated under the Dodd-Frank Act. The Talent and Compensation Committee reviewed factors, facts and circumstances regarding compensation consultant independence, including a letter from Pay Governance addressing Pay Governance and their consulting team’s independent status with respect to the following factors: (i) other services provided to us by Pay Governance; (ii) fees we pay to Pay Governance as a percentage of their total revenues; (iii) Pay Governance’s policies and procedures that are designed to prevent conflicts of interest;

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 25 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

(iv) any business or personal relationship between Pay Governance or members of their consulting team that serves the Talent and Compensation Committee and a member of the Talent and Compensation Committee; (v) any shares of our stock owned by Pay Governance or members of their consulting team that serves the Talent and Compensation Committee; and (vi) any business or personal relationships between our executive officers and Pay Governance or members of their consulting team that serves the Talent and Compensation Committee. After discussing these factors, facts and circumstances, the Talent Compensation Committee affirmed the independent status of Pay Governance and concluded that there are no conflicts of interest with respect to Pay Governance.

Talent and Compensation Committee interlocks and insider participation

No member of the Talent and Compensation Committee (i) was, during the year ended December 31, 2020,2022, or had previously been, an officer or employee of the company or (ii) had any material interest in a transaction with the company or a business relationship with, or any indebtedness to, the company. No interlocking relationships existed during the year ended December 31, 2020,2022, between any member of the Board or the Talent and Compensation Committee and an executive officer of the company.

Code of Ethics and Business Conduct and Governance Guidelines

The Board has adopted a code of ethics and business conduct that applies to all employees and directors. The Board has formalized policies, procedures and standards of corporate governance that are reflected in our Governance Guidelines.

Our Code of Ethics and Business Conduct outlines in great detail the key principles of ethical conduct expected of our employees, officers and directors, including matters related to conflicts of interest, use of company resources, fair dealing, and financial reporting and disclosure. The code establishes formal procedures for reporting illegal or unethical behavior to the company’s internal ethics committee. These procedures permit employees to report any concerns, including concerns about the company’s accounting, internal accounting controls or auditing matters, on a confidential or anonymous basis if desired. Employees may contact the ethics committee by email, in writing, by web-based report or by calling a toll-free telephone number. Any significant concerns are reported to the Audit Committee in accordance with the code.

|

|

Simultaneous Board service

Our director overboarding policy in our governance guidelines requirerequires that, if a director serves on three or more public company boards simultaneously, including our Board, a determination is made by our Board as to whether such simultaneous service impairs the ability of such member to effectively serve the company. Messrs. Fotiades andMr. Lyons and Ms. Kennard currently serve on at least three public company boards, including our Board. In each case, our Board has determined that such simultaneous board service does not impair the Board member’s ability to be an effective member of our Board.

Mr. Fotiades is the chief executive officer and a director of Cantel Medical Corp. He has advised us that he will no longer be CEO of Cantel Medical Corp. (or CEO in any other capacity) upon the closing of Steris Corporation’s acquisition of Cantel Medical Corp., expected to occur in the second quarter of 2021. Should the Steris acquisition terminate or not close, Mr. Fotiades will nevertheless retire as CEO of Cantel Medical Corp.

Certain relationships and related party transactions

We do not have any related party transactions to report under relevant SEC rules and regulations. According to our Articles of Incorporation, the Board may authorize any agreement or other transaction with any party even though one or more of our directors or officers may be a party to such an agreement or is an officer, director, stockholder, member or partner of the other party if: (i) the existence of the relationship is disclosed or known to the Board, and the contract or transaction is authorized, approved or ratified by the affirmative vote of not less than a majority of the disinterested directors, even if they constitute less than a quorum of the Board; (ii) the existence is disclosed to the stockholders entitled to vote, and the contract or transaction is authorized, approved or ratified by a majority of the votes cast by the stockholders entitled to vote (excluding shares owned by any interested director or officer or the organization in which such person is a director or has a material financial interest); or (iii) the contract or transaction is fair and reasonable to the company.

PROLOGIS PROXY STATEMENT | MARCH 24, 2023 | 26 |

| BOARD OF DIRECTORS AND CORPORATE GOVERNANCE |

We recognize that transactions between us and related parties can present potential or actual conflicts of interest and create the appearance that our decisions are based on considerations other than the company’s best interests and the best interests of our stockholders. Related parties may include our directors, executives, significant stockholders and immediate family members and affiliates of such persons.

Accordingly, several provisions of our code of ethics and business conduct are intended to help us avoid the conflicts and other issues that may arise in transactions between us and related parties, prescribing that:

| · |

|

| · |

|

| · |

|

| · |

|

These provisions of our code of ethics and business conduct may be amended, modified or waived by the Board or the Governance Committee, subject to the disclosure requirements and other provisions of the rules and regulations of the SEC and the NYSE.

No waivers of our code of ethics and business conduct were granted in 2020.2022.

Although we do not have detailed written procedures concerning the waiver of the application of our code of ethics and business conduct or the review and approval of transactions with directors or their affiliates, our directors would consider all relevant facts and circumstances in considering any such waiver or review and approval.

|

|

Biographies of our executive officers as of March 2021,2023, other than Mr. Moghadam, are presented below. Information for Mr. Moghadam is included above under “Board of Directors and Corporate Governance.” All ofMessrs. Moghadam, Arndt, Reilly, Anderson and Nekritz, along with Thomas S. Olinger, our executive officersformer CFO, are treated as named executive officers (each an “NEO”) for purposes of this proxy statement.

Thomas S. Olinger:Timothy D. Arndt

Chief Financial Officer

Years at Prologis: 18

Mr. Olinger, 54,Arndt, 50, has been our chief financial officer since May 2012April 2022 and was our chief integration officertreasurer from June 2011December 2013 to May 2012.April 2022. Prior thereto, Mr. Olinger wasArndt held various positions with the chief financial officercompany since joining AMB Property Corporation (“AMB”), Prologis’ predecessor company, in 2004, including as head of AMB from March 2007 to June 2011.corporate planning and as a part of the Company’s global deployment team. Prior to joining AMB, in February 2007, Mr. Olinger was the vice president and corporate controller at Oracle Corporation, an enterprise software company and provider of computer hardware products and services. Prior to his employment with Oracle, Mr. Olinger was an accountant and partner at Arthur Andersen LLP, where he served as the lead partner on our account from 1999 to 2002. Since January 2011, Mr. Olinger has served as a director of American Assets Trust, aworked in real estate investment trust investingstrategy at Gap Inc. and in office, retail and residential properties.debt capital markets at Forest City Enterprises. Mr. Olinger holds a Bachelor of Science in finance from the Kelley School of Business at Indiana University.

Eugene F. Reilly: Chief Investment Officer

Mr. Reilly, 59, has been our chief investment officer since March 2019. Mr. Reilly was our CEO, the Americas, from June 2011 until March 2019, and he served as president, the Americas, as well as a number of other executive positions, at AMB from October 2003 until the Merger in June 2011. Mr. Reilly serves on the technical committee of FIBRA Prologis, a publicly traded Mexican REIT that is sponsored and managed by the company. Prior to joining AMB in October 2003, Mr. Reilly was chief investment officer of Cabot Properties, Inc., a private equity industrial real estate firm of which he was also a founding partner. From August 2009 until December 2015, Mr. Reilly served as a director of Strategic Hotels and Resorts, an owner and asset manager of high-end hotels and resorts. Mr. Reilly holds an A.B. degree in economics from Harvard College.

Edward S. Nekritz: Chief Legal Officer, General Counsel and Secretary

Mr. Nekritz, 55, has been our chief legal officer, general counsel and secretary since the Merger in June 2011. Mr. Nekritz was general counsel of the Trust from December 1998 to June 2011 and secretary of the Trust from March 1999 to June 2011. Mr. Nekritz serves on the technical committee of FIBRA Prologis. Prior to joining the Trust in September 1995, Mr. Nekritz was an attorney with Mayer, Brown & Platt (now Mayer Brown LLP). Mr. Nekritz holds a Juris Doctor degreeArndt received his BBA from the University of Chicago Law SchoolToledo and an A.B. degree in governmentMBA from Harvard College.Cleveland State University. In addition, he completed the Stanford Executive Program at the Stanford Graduate School of Business.

Gary E. Anderson:Anderson

Chief Operating Officer

Years at Prologis: 28